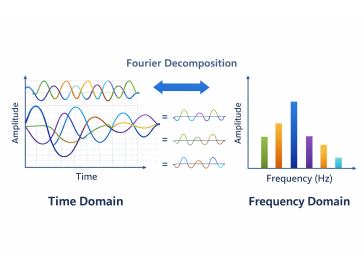

Frequency Domain, Spectral Analysis, Shock Persistence and Volatility, and Linearly Interpolated Time Series

In time series econometrics, I have studied cross-spectral properties of cointegrated time series, periodic properties of interpolated time series, shock persistence and output fluctuation of international time series, seasonal cycles & business cycles in the context of the inventory investment and output comovement, investment-saving comovement, spectral shapes of economic variables, interpolation and shock persistence of Prewar US macroeconomic time series, and the shock persistence and volatility properties of linearly interpolated low-order stationary and nonstationary time series.